We've another one of those laments, over at the Guardian, for the way in which the financial markets deliver financing to people who are poor. Apparently this is very bad, allowing poor people to finance capital expenditures in the same manner that we richer people are able to. You know, how nefarious Wall Street must be if it lets the poor, we mean really, poor people!, buy a car.

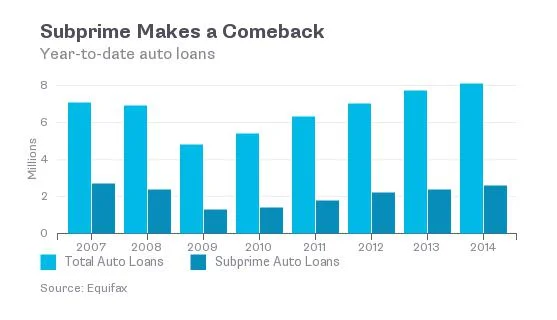

Many people are buying those cars with they help of Wall Street banks, which are lending money to people with bad credit again – just as they did prior to the financial crisis of 2007. In the last crisis, it was houses.The $26bn worth of subprime car loans is far short of the $500bn of subprime real estate securitization in 2006, at the top of the housing bubble, partly because cars are a lot cheaper than houses.

This time, like last time, Wall Street isn’t directly lending poor people money. That part is done by an array of smaller financial companies in strip malls and office parks.

The smaller financial companies sell the loans to Wall Street. Wall Street puts them into big piles, sorts them from weakest to strongest credit scores, and then sells the pieces and parts of them to their customers. The customers can be hedge funds in Greenwich, Connecticut, or other banks. No part of the loan goes unsold: from the highest rates to the lowest-rated, buyers are always there.

This process is called subprime securitization, and about $26bn of it will be done this year in auto loans to poor people.

This is, according to the author, just terrible. And of course the reality is that it's just wonderful.People who would not be able to afford a car can now do so: this enables them to get to work, to the shops, and thus makes them less poor. And the miracle here is that securitisation, the securitisation that distributes the risk.

Now it is possible, of course, to associate this subprime securitisation with what happened with subprime mortgage securitisation and thus wonder whether there's going to be a replay of 2008. But there won't be for two reasons. The first being that there's just not enough of these auto loans to cause anything like a systemic crisis.

The second is that it wasn't securitisation, nor subprime, that caused the problem last time around. It was fractional reserve banking: more specifically, that the slices and dices of these loans were on the books of banks who were leveraged in their holdings of them. So, when the value of the loans slid the banks became illiquid and possibly insolvent. If those same slices and dices had been in non-leveraged hands, pension and or insurance funds for example, then there wouldn't actually have been those runs on those banks.

So, all we're left with here with these subprime auto loans and their securitisation is that poor people get to buy cars more cheaply than they would without that spreading of the risk. And maybe The Guardian thinks that's terrible but the rest of us should regard it as a pretty good idea. We are, after all, the people who are pro-poor, aren't we?