For further comments or to arrange an interview, contact Head of Communications Kate Andrews: kate@adamsmith.org | 07584 778207.

- ‘Conspicuous consumption’ is no longer about buying flashy cars, clothes and jewellery to show their status—in fact this now signals lower status

- Today people are more likely to signal status with 'authenticity', environmentalism and knowledge

- This means luxury taxation and worries about a spiraling consumption arms race are out of place in the modern status economy, where ‘virtue signalling’ is an important phenomenon

- Subsidies for education should be reduced, since much of this activity is being pursued not for its inherent benefits, but to one-up others

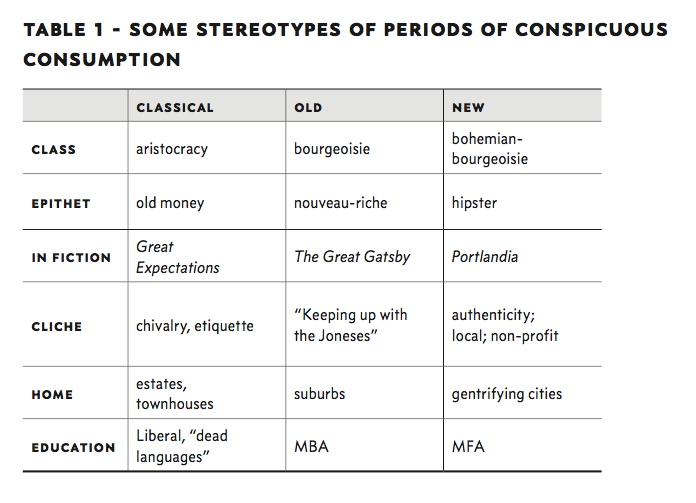

Virtue signalling has made widely-held ideas like ‘keeping up with the Joneses' and conspicuous consumption completely outdated, according to a new paper from the Adam Smith Institute. Rather than trying to one-up one another by buying Bentleys, Rolexes and fur coats, the modern social climber is more likely to try and show their ‘authenticity’ with virtue signalling by having the correct opinions on music and politics and making sure their coffee is sourced ethically, the research says.

The monograph, The New Aristocrats: A cultural and economic analysis of the new status signalling by Prof. Ryan Murphy of Southern Methodist University in Texas, lays out how trends in status signalling—showing one’s self to be worthy of respect and privilege in the eyes of one’s group—have changed over recent decades.

While the conventional understanding holds that families are apt to buy ever-bigger cars and ever-bigger homes in the pursuit of higher social rank—a fruitless zero-sum competition that might well be tackled by luxury taxes—the new race for prestige is quite different.

A modern aspirant elitist would be better off getting an arts degree than buying a gas-guzzling four-by-four, Prof. Murphy points out, if they want to raise their profile in the eyes of their peers. This trend of ‘virtue signalling’ has been widely noted, but policy has not shifted with society.

Education is one policy where Murphy’s analysis is readily applicable. Though pursuing practical education, a STEM degree, or even building up work experience may be better for an individual’s earnings and society’s productivity, individuals may pick extended study of essentially useless degrees in pursuit of status.

This is enabled by an extensive system of subsidies, which actually, since the last reforms, made the terms for those expecting to earn very little—i.e. those pursuing degrees that barely enhanced their career potential—much more generous. Murphy’s analysis suggests these subsidies should be scaled back—we are only encouraging an endless arms race.