Tim Worstall 18/05/2017 Tim Worstall 18/05/2017 The demands become ever more extreme, of course they do Read More Tim Worstall 17/05/2017 Tim Worstall 17/05/2017 Excess diesel NOX emissions cause 0.07% of deaths globally Read More Sam Bowman 16/05/2017 Sam Bowman 16/05/2017 How did France's Robin Hood Tax work out? Read More Madsen Pirie 16/05/2017 Madsen Pirie 16/05/2017 The great bidding war Read More Tim Worstall 16/05/2017 Tim Worstall 16/05/2017 Another example of something we've long maintained to be true Read More Tim Worstall 15/05/2017 Tim Worstall 15/05/2017 A bigger NHS budget wouldn't solve the ransomware problem, no Read More Tim Worstall 14/05/2017 Tim Worstall 14/05/2017 Something that puzzles us deeply about the Labour Party Manifesto Read More Tim Worstall 13/05/2017 Tim Worstall 13/05/2017 The problem with over arching regulation is that it concentrates error Read More Richard Teather 12/05/2017 Richard Teather 12/05/2017 The effect of Labour's corporation tax Read More Tim Worstall 12/05/2017 Tim Worstall 12/05/2017 Maybe there are just too many such graduate teachers? Read More Preston Byrne 11/05/2017 Preston Byrne 11/05/2017 Cryptocurrency is interesting again Read More Sam Dumitriu 11/05/2017 Sam Dumitriu 11/05/2017 Taking innovation seriously Read More Newer Posts Older Posts Your subscription could not be saved. Please try again. Your subscription has been successful. Blogs by email Enter your email address to subscribe I agree to receive your newsletters and accept the data privacy statement. SUBSCRIBE

Tim Worstall 18/05/2017 Tim Worstall 18/05/2017 The demands become ever more extreme, of course they do Read More

Tim Worstall 17/05/2017 Tim Worstall 17/05/2017 Excess diesel NOX emissions cause 0.07% of deaths globally Read More

Tim Worstall 16/05/2017 Tim Worstall 16/05/2017 Another example of something we've long maintained to be true Read More

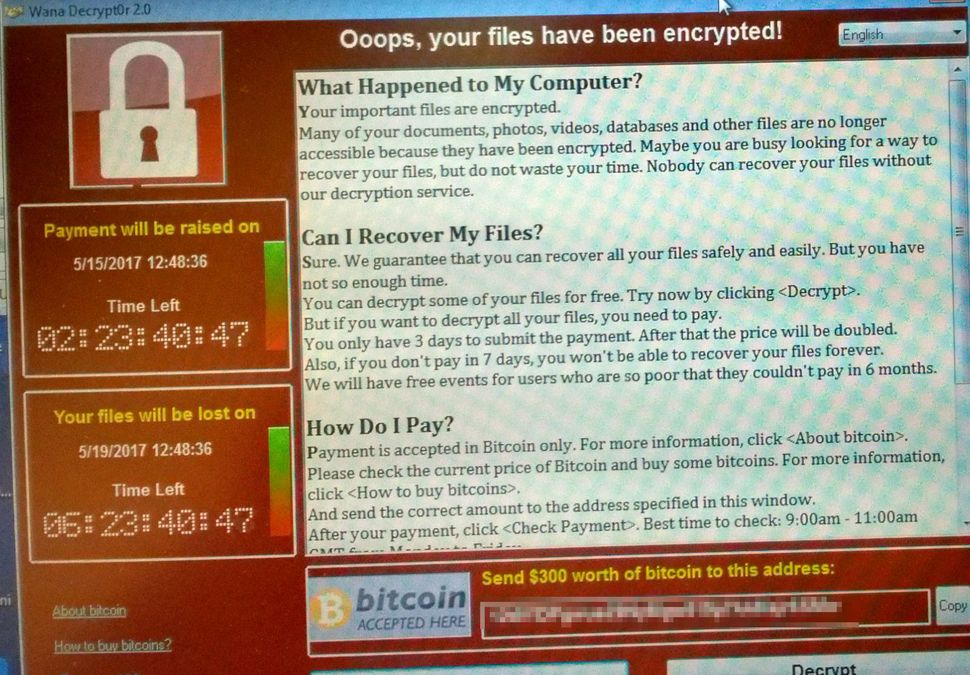

Tim Worstall 15/05/2017 Tim Worstall 15/05/2017 A bigger NHS budget wouldn't solve the ransomware problem, no Read More

Tim Worstall 14/05/2017 Tim Worstall 14/05/2017 Something that puzzles us deeply about the Labour Party Manifesto Read More

Tim Worstall 13/05/2017 Tim Worstall 13/05/2017 The problem with over arching regulation is that it concentrates error Read More

Richard Teather 12/05/2017 Richard Teather 12/05/2017 The effect of Labour's corporation tax Read More

Tim Worstall 12/05/2017 Tim Worstall 12/05/2017 Maybe there are just too many such graduate teachers? Read More