Money & Banking Charlotte Bowyer 29/09/2014 Money & Banking Charlotte Bowyer 29/09/2014 What's happened to the 'Bitcoin Revolution?' Read More International Tim Worstall 29/09/2014 International Tim Worstall 29/09/2014 Isn't Will Hutton's logic here just so lovely? Read More Economics Tim Worstall 28/09/2014 Economics Tim Worstall 28/09/2014 Getting it entirely wrong on fatcat CEO pay Read More Economics Tim Worstall 27/09/2014 Economics Tim Worstall 27/09/2014 On Unite's demand for a £1.50 rise in the minimum wage Read More Tax & Spending Kate Andrews 26/09/2014 Tax & Spending Kate Andrews 26/09/2014 UKIP is on the right track to beat low pay Read More Money & Banking Tim Worstall 26/09/2014 Money & Banking Tim Worstall 26/09/2014 Colin Hines and the Magic Money Tree Read More Education Tim Worstall 25/09/2014 Education Tim Worstall 25/09/2014 Trying to explain the American academic jobs market Read More Economics Ben Southwood 24/09/2014 Economics Ben Southwood 24/09/2014 Everything's coming up monetarist! Read More Planning & Transport Tim Worstall 24/09/2014 Planning & Transport Tim Worstall 24/09/2014 It really is the planning system that's harming us Read More Politics & Government, Regulation & Industry Philip Salter 23/09/2014 Politics & Government, Regulation & Industry Philip Salter 23/09/2014 The visa and the sausage Read More Healthcare Tim Worstall 23/09/2014 Healthcare Tim Worstall 23/09/2014 On Ed Miliband's new tax on tobacco profits Read More Energy & Environment Kate Andrews 23/09/2014 Energy & Environment Kate Andrews 23/09/2014 Why Miliband is wrong on energy policy Read More Newer Posts Older Posts Your subscription could not be saved. Please try again. Your subscription has been successful. Blogs by email Enter your email address to subscribe I agree to receive your newsletters and accept the data privacy statement. SUBSCRIBE

Money & Banking Charlotte Bowyer 29/09/2014 Money & Banking Charlotte Bowyer 29/09/2014 What's happened to the 'Bitcoin Revolution?' Read More

International Tim Worstall 29/09/2014 International Tim Worstall 29/09/2014 Isn't Will Hutton's logic here just so lovely? Read More

Economics Tim Worstall 28/09/2014 Economics Tim Worstall 28/09/2014 Getting it entirely wrong on fatcat CEO pay Read More

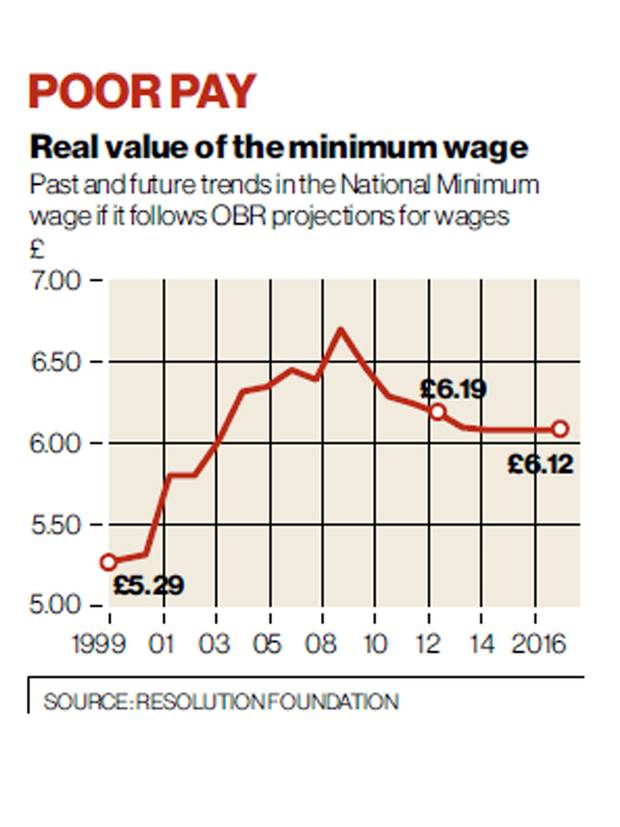

Economics Tim Worstall 27/09/2014 Economics Tim Worstall 27/09/2014 On Unite's demand for a £1.50 rise in the minimum wage Read More

Tax & Spending Kate Andrews 26/09/2014 Tax & Spending Kate Andrews 26/09/2014 UKIP is on the right track to beat low pay Read More

Money & Banking Tim Worstall 26/09/2014 Money & Banking Tim Worstall 26/09/2014 Colin Hines and the Magic Money Tree Read More

Education Tim Worstall 25/09/2014 Education Tim Worstall 25/09/2014 Trying to explain the American academic jobs market Read More

Economics Ben Southwood 24/09/2014 Economics Ben Southwood 24/09/2014 Everything's coming up monetarist! Read More

Planning & Transport Tim Worstall 24/09/2014 Planning & Transport Tim Worstall 24/09/2014 It really is the planning system that's harming us Read More

Politics & Government, Regulation & Industry Philip Salter 23/09/2014 Politics & Government, Regulation & Industry Philip Salter 23/09/2014 The visa and the sausage Read More

Healthcare Tim Worstall 23/09/2014 Healthcare Tim Worstall 23/09/2014 On Ed Miliband's new tax on tobacco profits Read More

Energy & Environment Kate Andrews 23/09/2014 Energy & Environment Kate Andrews 23/09/2014 Why Miliband is wrong on energy policy Read More