There's some serious idiots out there

So, another one of these attempts to make clothes only from local ingredients. Rather ignoring much of the human history of trade which has seen extensive trade in textiles and clothing pretty much ever since human beings started wearing them. But sure, why not experiment?

In December, just under 2,000 limited-edition oatmeal-colored cotton hoodies cropped up at The North Face’s online and brick-and-mortar stores, commanding a premium price of $125 each. By January, the hoodies were sold out.These shirts spun an interesting tale. They were an experiment by the sports clothing company to see if everything it needed to produce the hoodie — from the cotton to the finished garment — could be found within 150 miles of its headquarters in the San Francisco Bay Area.

Well, they couldn't do it but so what. A market economy is that continual succession of experiments, we cast off the ones that fail. However, here's where the ignorance of what is staring one in the face comes in:

The North Face hoodie was part of its Backyard Project, which is part of the company’s effort to work closely with the US textile industry, from farmers to factories, to use sustainably grown materials and reduce waste.

Reduce waste is a synonym for using fewer resources to create a particular output. And we've already got a system to do this: it's called that market and those prices. At which point it's terribly simple to work out whether such localism reduces resource consumption.

These "local" hoodies cost that $125. The standard, non-local hoodies by the same company cost $45 to $55. Making the entirely reasonable assumption that they're applying the same standard mark up to both products this means that the local version consumes more than twice as many resources as the non-local one.

We can work out resource use just by looking at prices.

Intellectual property: in search of real evidence

There are many problems with economic research on the costs and benefits of intellectual property protections. For one, the most common measure of research output is the rate of patenting; but changing the strength of patents both changes the incentives over doing research and the incentives over patenting that research, introducing a huge bias.

For another, a lot of what you want to measure is pure counterfactual: what would have happened under a different (i.e. stronger or weaker) intellectual property system—but how can we track research that might have happened but didn't actually? There is little info kept on, for example, promising drug compounds that pharmaceutical firms never followed up on.

A third is that patent laws are fairly uniform within countries. Where they vary in practice across areas the industries are often too variegated to accurately compare. There are some variations across the developed world, but aside from the fact that countries systematically vary in relevant ways, small changes in individual countries' policies are rarely big enough to matter. If Denmark changes its standard term length from 17 to 20 years this has very little impact on the incentives international firms face.

Canny researchers have tried to get around some of these problems. For example Lerner (2009) looks at the impact tighter patent protection in Austria has on patenting by Austrians who live in the UK. Though stricter patent provisions did lead to more patenting within a country, it was not associated with extra patenting by nationals abroad.

Other research has attempted to measure total Research & Development spending, total scientific papers published, total citations to scientific papers, or even clinical trials and drug approvals, in order to get a better grip on the actual pace of innovation.

A highly interesting new NBER paper by Heidi L. Williams at MIT, entitled "Intellectual Property Rights and Innovation: Evidence from Healthcare Markets" (pdf) lucidly explains these problems and the standard framework for economic research on intellectual property. Viz: does the free market under-provide research without IP? Do the benefits IP rights generate in terms of extra innovation outweigh the costs of restricting an idea's use for 20 years or more?

Williams manages to identify a variation between the delay in commercialising early-stage and late-stage cancer treatments, and hence the effective length of the patent (even though the statutory length is the same). Firms patent when they discover things, not when they commercialise them, and this means that the length of Federal Drug Agency trials and other hold-ups influence how long they actually get a monopoly on a drug's sale. In this context, late-stage cancer drugs are often rushed to market, whereas early-stage cancer drugs take longer to approve (and hence firms get a shorter effective patent).

Williams finds that shorter commercialisation lags lead to more investment in innovation in that area.

Taking advantage of our surrogate endpoint variation, we estimate counterfactual R&D allocations and induced improvements in cancer survival rates that would have been observed if commercialization lags were reduced. Our back-of-the-envelope calculation suggests that the distortion of private research dollars away from long-term projects has quantitatively important implications for the survival outcomes of US cancer patients: we estimate that among one cohort of patients - US cancer patients diagnosed in 2003 - longer commercialization lags generated around 890,000 lost life-years. Valued at $100,000 per life-year lost (Cutler, 2004), the estimated value of these lost life-years is on the order of $89 billion for this single cohort of patients.

Pretty strong results for IP advocates, but more importantly a very promising avenue for further research.

We shouldn't have to care who has political power

An extremely good point made by Scott Sumner:

I consider myself to be reasonably well informed. I generally know which party is in power in countries like Sweden. And yet at no time in my life could I name a single Swiss political party, or political figure. There's a lesson there somewhere. Perhaps the lesson is that you don't want to live in a country where it matters a lot who gets elected President.

Our knowledge of Swiss politics is similarly deficient. We're not even sure if they have a party political system. Yet it does have to be said that the country runs pretty well. So perhaps the agonising that we have to do over who does gain political power here is what the problem actually is. Our recent ability to chose between a scion of the haute bourgeoisie and a man intellectually bested by a bacon sandwich may not have been the most edifying spectacle, but the problem is that we had to worry about it at all.

The point about politics is to come up with some method of getting the bins taken out. And that's a reasonably simple task and one that the Swiss most definitely have a handle upon. It's also necessary to have someone called "the government" simply because visiting dignitaries expect there to be one. But over and above that the place that seems to be governed best is the one where pretty much no one pays any attention to who is governing simply because it's not very important who is. Because politics simply doesn't intrude much into anyones' life.

We recommend it as a system. Anything important can be decided by the people in referenda, there's a bit of bureaucracy necessary and then let people just get one with things as they wish. Something of a plan, eh?

Magna Carta - and EU law today?

Lord Sumption has been telling the papers that we owe our freedoms more to the French Revolution and its Declaration of Rights than to Magna Carta, the 800th anniversary of which we celebrate this month. He is wrong. But each passing day makes him more right, and that is the whole problem. A real problem for freedom, not some merely smug debating point. Sumption may be a distinguished mediaeval historian, but he is a poor political economist, or legal scholar for that matter. He calls the Charter a 'turgid' document of its time, and says it has 'nothing to do' with our libertarian tradition.

He is right that it reads like something rather turgid and technical. It was indeed mainly a list of demands, and was never meant as a constitution. But what it demands is critical to the development of limited government and representative democracy in the centuries that followed.

Magna Carta is the re-assertion of property rights that Anglo-Saxon England enjoyed before the Norman Conquest. The limits it imposes on authority – preventing the King's arbitrary confiscation of people's property and freedom – occupy only three or four of its 63 clauses and are therefore easily dismissed by those who think the Charter was just a hotchpotch of 'trade union' demands by the aristocracy.

But those who drew up the Charter knew that these few clauses are absolutely crucial. They are there precisely to guarantee those property rights that are spelled out in the rest of the document. What good is it to have rights if they are unenforceable because the authorities can act without restraint.

From that assertion of property rights, grows parliamentary democracy. Sure, as Sumption sneers, the Charter is by no means a democratic constitution, and concerns itself only with the rights of a rich few. But it reasserted the pre-Norman tradition that the rules of taxation and justice should be based on agreement, not on the whim of monarchs. To reach agreement, you need debate. And to debate, you need some kind of representative parliament.

It also explains England's later history as a great trading nation, and the entrepreneurial flair that abides in the Anglophone nations. The Charter guaranteed property rights, and that principle was quickly expanded from just the nobility to everyone. So people could build up capital without fear of being expropriated by kings, ministers and officials.

And the common law that was reasserted by the Charter allows people to do what they want, provided only that others are not harmed by it. Top-down Continental law, by contrast, requires you to seek official permission first. It is obvious which one is likely to encourage more innovation.

Sumption also tries to show the Charter's irrelevance by dismissing its insistence that justice should be based on the 'law of the land'. The assertion as worthless, he says, because the King decided what the law actually was. But the whole point was that the Charter reasserted the commonly agreed fact that the 'law of the land' was much older and more fundamental than King-made law. It was the common law of the Anglo-Saxons, built up, by the common people over centuries. This law had evolved and endured, despite the efforts of feudal authorities to supplant it, because it worked and because it was made by the people as they went about their everyday business. This common law was a matter for everybody, not just for the king to decide and hand down to everyone else.

We have the same issues today, with Britain's common law tradition being swamped by top-down law in the shape of EU regulation. Here again, the Continental tradition that you need detailed regulation that says what you can do is at odds with Britain's common law approach that you are free to act as you choose unless there is some proven and agreed reason not to.

The difference is crucial, and that is why Sumption is so horribly wrong to suggest that our libertarian tradition owes more to France than to Runnymede. Perhaps our rights and freedoms are indeed being subjected more and more to this Continental legal tradition. But this legal harmonisation is something to be mourned and feared, not celebrated.

The long history of school choice division

Most people, acting rationally, would prefer to choose the school their child goes to as opposed to having their child forcibly assigned to a school. So opposition to school choice seems no less strange wherever it comes from. Nonetheless understanding the reasons is enlightening. The divide of opinion on school vouchers in the States, for example, is portrayed as being between the left and the right. Or Republicans against Democrats and whites against minorities. But it is not as simple as this and not really the case. A new paper (pdf) by Shuls and Wolf studies the empirical reality regarding the political and racial divide over vouchers and explains its history in the U.S to offer conclusions about the logic of political support of and opposition to school choice. It also explains, for the unacquainted, what we mean when we talk about private school choice.

These two charts demonstrate the rise and prevalence of Private School Choice Programs in the States today:

The interesting finding is that while support for vouchers does tend to be higher among Republicans, support at the policymaking level is found both among ideological Democrats of the social-justice-promoting kind like Senator Corey Booker, and Republicans like Senator Rand Paul who support free markets. Those opposed tend to be moderate and mostly rural Republicans and establishment Democrats.

Teachers’ unions contribute more money than any other interested party to election candidates in the U.S. Of their campaign contributions, 88-99% of national-level, and 80-90% of state-level, contributions have gone to Democrats. The priority policy issue for the main teaching unions – the National Education Association and (NEA) and the American Federation of Teachers (AFT) – is to stop the spread of private school choice. Therefore one reason why so many Democrats may actually be opposed to school choice is that they would be doing so in spite of their single largest funder.

On the contrary, one has to ask why elected politicians in the U.S would support private school choice given teaching unions’ opposition. Research conducted for the Friedman Foundation for Educational Choice found 40% of parents polled would prefer to send their child to a private school and 10% of respondents would rather a public charter school. Private school vouchers were supported by 63% of respondents.

As DiPerna reports, “The demographic groups having the highest positive margins and most likely to favor school vouchers are school parents (+42 points), Southerners (+36 points), Republicans (+42 points), young voters (+44 points), low-income earners (+47 points), African Americans (+50 points), and Latinos (+47 points)” (DiPerna 2014, p. 14).

Reports from parents are far-off actual enrolment figures. The National Center for Educational Statistics tells us 9% of K-12 students attend private schools and 4% attend charter schools. So the Friedman Foundation poll suggests that opposition from the unions is pitted against popular opinion, especially in areas with more young people and ethnic minorities.

Inspired by the Prisoner's Dilemma, the School Choice Dilemma explains some of this by illustrating the compelling reasons for the opposition and support found in various political factions. Imagine two groups of students, one "advantaged" and one "disadvantaged"; one has enjoyed educational trips, access to materials and so on and the other hasn't. When both are given the opportunity to either accept their assigned school or to choose it themselves, they will be impacted in different ways.

If they both accept the assigned school, then there will be a mix of advantaged and disadvantaged students, which benefits (B) the disadvantaged from integrating with a brighter peer group; but may actually harm (H) the advantaged. Compared to this, the diagram shows that both will have an incentive to 'defect' and move to a situation where only they get S—the benefit of school choice. Advantaged students can already do this by buying houses near good schools or going to private schools—but the disadvantaged achieve this through targeted vouchers.

The conclusion is that we will probably continue to see rational politicians from both sides oppose school choice as the establishment in both parties have strong political incentives for protecting the status quo. Meanwhile social-justice politicians see school choice as a means to improving educational outcomes for disadvantaged students, and free-market individuals see school choice as a fundamental way to make education more efficient.

Quite right, we should abolish stamp duty on shares

As ever when there's a budget in the offing we've people making suggestions about what should be in said budget. Some of these suggestions are even sensible, as is this one arguing that we should abolish stamp duty on shares:

“Abolishing the tax would lead to an immediate 7.7pc, or £133bn, increase in the value of listed companies on the LSE’s main market on the day of abolition,” he wrote. “It would incentivise saving for the future, removing a £402m a year burden from UK pension schemes and reduce the tax liability by up to £18,000 from the average UK family’s savings.”

A previous academic look into the subject is here.

The important thing to understand is the incidence of this tax. Certainly, it's the people buying and selling shares that appear to pay the tax itself. But after everything has flowed through the economy who is it that actually bears the economic cost of its existence? One answer is as above, pension funds. The end result is that pensions are lower than they would be in the absence of this tax. And, given that we tax privilege pensions in the first place it seems most odd to have another tax which then reduces them.

The other group who lose out is the workers in the country in general. As is noted above share prices would rise in the absence of the tax. This is equal and equivalent to making capital cheaper for companies. Cheaper capital will mean more capital being employed. And it's the addition of capital to labour that increases productivity, the average productivity of labour being what determines the average wages in the economy. Thus more expensive capital lowers average wages.

A tax which both lowers pensions and also wages in general doesn't seem to have a lot going for it. So, yes, we agree, abolish stamp duty on shares.

The problem with identities in economics

Obviously, George Osborne's plan to make budget deficits illegal is just a piece of politicking. For it's only "illegal in certain circumstances" and being in a recession is a special circumstance. So, actually, it's really just a restatement of the Keynesian orthodoxy, that there should (can be if you prefer) be fiscal stimulus in a recession and there should also be fiscal austerity in the boom so as to reduce the white hot heat of that technological revolution. Shrug. But it's got all the right people het up as this letter to The Guardian tells us:

Economies rely on the principle of sectoral balancing, which states that sectors of the economy borrow and lend from and to each other, and their surpluses and debts must arithmetically balance out in monetary terms, because every credit has a corresponding debit. In other words, if one sector of the economy lends to another, it must be in debt by the same amount as the borrower is in credit. The economy is always in balance as a result, if just not at the right place. The government’s budget position is not independent of the rest of the economy, and if it chooses to try to inflexibly run surpluses, and therefore no longer borrow, the knock-on effect to the rest of the economy will be significant. Households, consumers and businesses may have to borrow more overall, and the risk of a personal debt crisis to rival 2008 could be very real indeed.

This is true, in one model, because that's how we set that one model up. Indeed, it's how we define that model. But we must not confuse the model with the economy, nor the map with the territory. For there's no particular reason why there has to be inter-sectoral lending or borrowing at all. There can, obviously, be intra-sectoral such. Some companies are cash rich at present. Some households are at that stage of life where they have significant savings and or assets. Some companies desire borrowing, as do some households. There's no reason at all why there must be lending or borrowing across those sectoral boundaries, nor why government should be taking any part in any that does happen. It's simply a construct of our model that we think it must. And, again, models are not reality.

Our economists are getting rather carried away by the constraints of the models they're using. But then, a group letter to The Guardian signed by Andrew Simms, Richard Murphy and Howard Reed. We knew it was going to be wrong, didn't we?

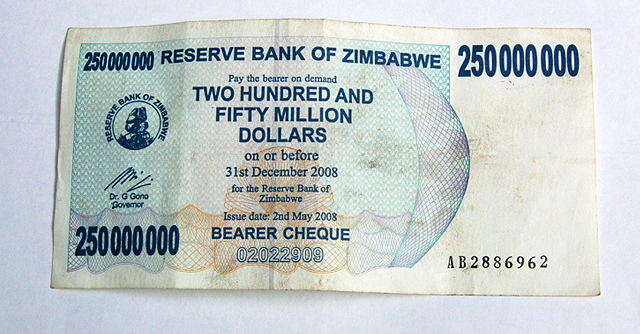

There's a lot of ruin in a nation

But ruin is not something in infinite supply in any nation:

From Monday, customers who held Zimbabwean dollar accounts before March 2009 can approach their banks to convert their balance into US dollars, the governor of the Reserve Bank of Zimbabwe, John Mangudya, said in a statement.

Zimbabweans have until September to turn in their old banknotes, which some people sell as souvenirs to tourists.

Bank accounts with balances of up to 175 quadrillion Zimbabwean dollars will be paid $5. Those with balances above 175 quadrillion dollars will be paid at an exchange rate of $1 for 35 quadrillion Zimbabwean dollars.

The highest – and last – banknote to be printed by the bank in 2008 was 100tn Zimbabwean dollars. It was not enough to ride a public bus to work for a week.

The bank said customers who still had stashes of old Zimbabwean notes could walk into any bank and get $1 for every 250tn they hold. That means a holder of a 100tn banknote will get 40 cents.

At some point simply running the printing presses does run into real problems. Our favourite little story from this whole disastrous episode comes from the final end days of the printed currency. Normally, currency printing is a very profitable occupation. Bit of paper, the price of some ink, and a banknote that is worth whatever the government says it is is created. Right at the end there it's said that the final decision to stop printing was taken because....no one would accept a bank note of any denomination at all, or any number of them, in return for supplying the ink with which to print the banknotes.

There have been hyperinflations before and it's a near certainty that it will happen again, somewhere. But this is the only example we know of where seigniorage was ridden all the way down to the bottom, to the bitter end.

The public wealth of nations

In 2013's Cash in the Attic ASI fellow Nigel Hawkins detailed £600bn of assets the government owned, but had never subjected to a market test. The paper recommended selling 10% of the assets off to begin with, in order to subject them to the market test and see if they were being best used, as well as giving the government money to reduce the national debt A new book, The Public Wealth of Nations, written by Dag Detter and Stefan Fölster, argues a lot of the same points—although with a much broader scope and deeper focus. The book's blurb runs:

When you look around the world it's almost as if Thatcher/Reagan economic revolution never happened. The largest pool of wealth in the world – a global total that is twice the world's total pension savings, and ten times the total of all the sovereign wealth funds on the planet – is still comprised of commercial assets that are held in public ownership.

And yet, while this is the largest pool of assets in the world, is also one of the murkiest – what goes on inside them is often not even properly known by the governments who own them. In most countries this vast portfolio is both a fiscal and political burden on society. If professionally managed it could generate an annual yield of 2.7 trillion dollars, more than current global spending on infrastructure: transport, power, water and communications.

Is there any reason why hospitals should own their buildings rather than rent them with long-term contracts? Outside of some historically-significant places couldn't the same be said for most public property. And how do we know whether an army barracks is well-placed if the army doesn't compete with other users over it?

The authors recapitulate their argument in a Citigroup note (pdf), with an introduction by Willem Buiter, going over their case for turning over government property to a properly-managed sovereign wealth fund.

As ever, the ASI is ahead of the curve!

Backing the 1%

I spoke last Thursday in the Cambridge Union on the motion, "This House Believes We Need the Richest 1%." I spoke in favour, giving 6 reasons for my support.

1. The richest 1% feature many people who have provided things to improve our lives.

These include Google, Amazon, Facebook, Paypal, YouTube, etc. We use them regularly and have propelled their developers into the top 1%. They made life easier, more interesting & more rewarding by providing services of value to others. Even the much-derided bankers have made capital work more effectively and made it more available.

2. The richest 1% act as an example to others.

People look at the careers of Elon Musk, Bill Gates, Steve Jobs, & Mark Zuckerberg, and are themselves inspired to develop goods and services that will similarly be of use and value to others.

3. The top 1% pay taxes.

In the UK the 1% pay nearly 30% of all income tax. The top 3,000 UK earners pay more between them than the bottom 9 million. Their taxes support schools, hospitals and essential public services.

4. They give to charitable causes.

They are the mainstay of many medical & cultural charities. They fund art galleries, museums & symphony orchestras. They are helping to conquer disease and suffering. The Bill and Melinda Gates Foundation is funding the eventual conquest of malaria, a disease that kills an estimated 2m people annually, including 500,000 children. Warren Buffet has issued the Giving Pledge, for rich people who pledge to give or leave half their fortunes to charity. Hundreds, including Bill Gates, have signed it.

5. The top 1% are early adopters.

They can afford to buy the new gadgets and try out the new processes. The ones that fall short of expectations drop by the wayside, but successful ones go into mass production, fall in price and become generally available. It was the 1% who bought the first large flat screen plasma and LCD TVs that are now commonplace and within reach of most people.

6. The top 1% include those who accelerate the pace of technological advance by putting their money behind adventurous developments.

Paul Allen made his fortune with Microsoft, and put $25m to back SpaceShipOne, winner of the X-Prize for the first private vehicle to carry people into space. Elon Musk made his fortune from Paypal, and used it to fund Tesla because he believes that electric cars can enable a cleaner world. He funded SpaceX, which sends Dragon capsules to the Space Station and is testing ways of landing and refueling its boosters. He does this to speed up accessible spaceflight.

With more time I could have added more reasons, such as the fact that the 1% help create most of the new jobs that replace ones automated or outsourced. I concluded by saying that the 1% help make the world a better, more colourful and more interesting place, and that the goods and services they make available enrich our lives.