Bureaucracy gone mad we tell ‘ee

An underlying and fundamental part of our analysis of what has gone wrong with this sceptered isle is that we simply have too much bureaucracy.

So, where’s the beef here?

Waitrose has ruled out buying American beef and chicken as it insisted it would stand “shoulder-to-shoulder with our farmers” after Sir Keir Starmer’s US trade deal.

Regulation has its own Laffer Curve

That is, it’s possible to regulate something so much that the protections aimed at disappear.

After the Rose Garden 6 - Foreign policy

This week’s post takes foreign policy as first serving the people of the UK, then our friends, then the rest of the world. Once this was known as “realism”.

The latest environmental demand - don’t trade with poor people

We do - no really, we do - wonder what goes through minds like these: UK urged not to exploit poor countries in rush for critical minerals

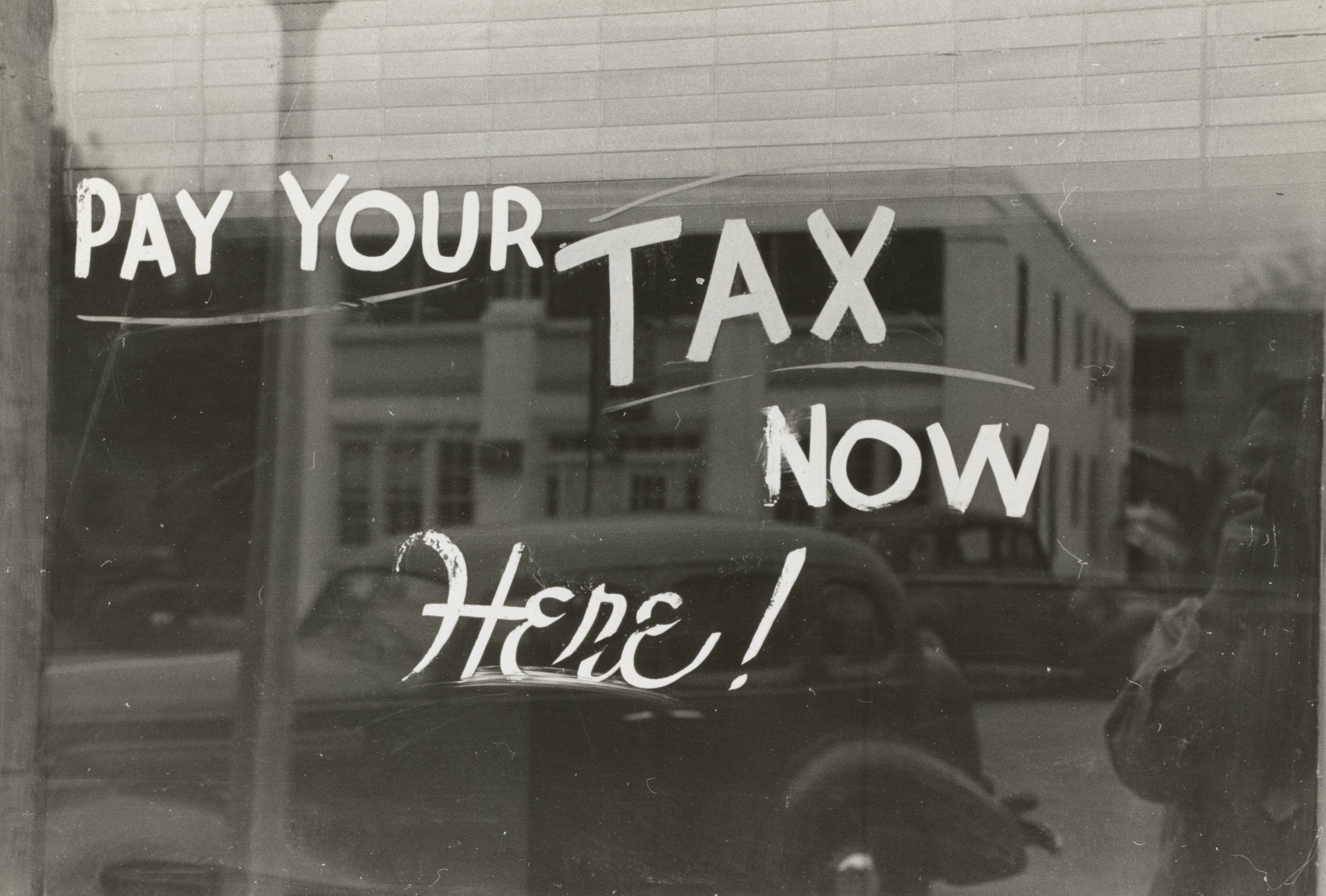

Why tax the poorest?

There is a strong case for proposing that those living on the basic UK State Pension or the National Minimum Wage should be exempt from income tax and National Insurance contributions (NICs).

It’s not obvious that nationalisation would solve water shortages

We await the usual insistences as a result of this story: Thames Water refuses to rule out a hosepipe ban as drought looms.

Taxation is theft, of course

Taxation is collected under the threat of punishment such as fines, asset seizure, or imprisonment, making it non-consensual.

Why not repeal the Dodd Frank conflict minerals rules?

One of those differences between political, bureaucratic, action and markets. In a market environment the Dodd Frank rules on conflict minerals would be dead and buried now.

Celebrating Trafalgar Day

My colleague, Dr Eamonn Butler, will not like this proposal at all because he has expressed the view that Bank holidays are an anachronism that should be abolished, although he did once grudgingly tell the ASI staff that they could take Christmas morning off.

But what if AI and the robots do take all our jobs?

The only correct answer to that question is that we’re all as rich as Croesus.

NHS debit cards

One idea to improve UK national healthcare has been the proposal to give everyone an NHS debit card they could use to access private treatment if the NHS delay in treating them were deemed unacceptably long.