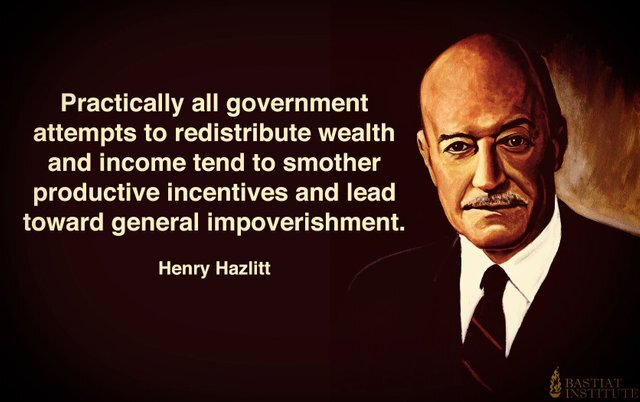

Tim Worstall 01/12/2019 Tim Worstall 01/12/2019 The quite appalling level of private contracts in the NHS Read More Madsen Pirie 30/11/2019 Madsen Pirie 30/11/2019 Winston Churchill Read More Tim Worstall 30/11/2019 Tim Worstall 30/11/2019 How much do we owe the rest of the world over climate change? Read More Madsen Pirie 29/11/2019 Madsen Pirie 29/11/2019 Compulsory education Read More Tim Worstall 29/11/2019 Tim Worstall 29/11/2019 The BMJ on the NHS - Depends upon which numbers you use really Read More Madsen Pirie 28/11/2019 Madsen Pirie 28/11/2019 Hazlitt and Engels Read More Tim Worstall 28/11/2019 Tim Worstall 28/11/2019 The engineers are entirely correct here about climate change Read More Madsen Pirie 27/11/2019 Madsen Pirie 27/11/2019 The early dawn of helicopter money Read More Charlie Paice 27/11/2019 Charlie Paice 27/11/2019 Young people and immigrants will be hit hardest by Labour's rent controls Read More Tim Worstall 27/11/2019 Tim Worstall 27/11/2019 Money where mouth is - in praise of Ben Lovett of Mumford & Sons Read More Luke Gardiner 26/11/2019 Luke Gardiner 26/11/2019 The other costs of nationalisation Read More Shradha Badiani 26/11/2019 Shradha Badiani 26/11/2019 In praise of VAT Read More Older Posts Your subscription could not be saved. Please try again. Your subscription has been successful. Blogs by email Enter your email address to subscribe I agree to receive your newsletters and accept the data privacy statement. SUBSCRIBE

Tim Worstall 01/12/2019 Tim Worstall 01/12/2019 The quite appalling level of private contracts in the NHS Read More

Tim Worstall 30/11/2019 Tim Worstall 30/11/2019 How much do we owe the rest of the world over climate change? Read More

Tim Worstall 29/11/2019 Tim Worstall 29/11/2019 The BMJ on the NHS - Depends upon which numbers you use really Read More

Tim Worstall 28/11/2019 Tim Worstall 28/11/2019 The engineers are entirely correct here about climate change Read More

Charlie Paice 27/11/2019 Charlie Paice 27/11/2019 Young people and immigrants will be hit hardest by Labour's rent controls Read More

Tim Worstall 27/11/2019 Tim Worstall 27/11/2019 Money where mouth is - in praise of Ben Lovett of Mumford & Sons Read More