Tim Worstall 20/11/2018 Tim Worstall 20/11/2018 Once again, to miss the point about health care treatment costs Read More Ananya Chowdhury 19/11/2018 Ananya Chowdhury 19/11/2018 An Enquiry Concerning Human Urban Planning Read More Tim Worstall 19/11/2018 Tim Worstall 19/11/2018 To explain the UN Rapporteur on UK Extreme Poverty Read More Joshua Curzon 18/11/2018 Joshua Curzon 18/11/2018 Venezuela Campaign: building crisis cements Maduro's failed legacy Read More Tim Worstall 18/11/2018 Tim Worstall 18/11/2018 Health care is a luxury so of course Americans spend more upon it Read More Tim Worstall 17/11/2018 Tim Worstall 17/11/2018 What is the correct number of bank branches? Read More Madsen Pirie 16/11/2018 Madsen Pirie 16/11/2018 Wider applications of the Kuznets Curve Read More Tim Worstall 16/11/2018 Tim Worstall 16/11/2018 It's the decision making process itself which is wrong here Read More Tim Worstall 15/11/2018 Tim Worstall 15/11/2018 It's the disinformation from some that so annoys about climate change Read More Tim Worstall 14/11/2018 Tim Worstall 14/11/2018 At last, an accurate description of Gordon Brown's personal income tax policies Read More Tim Worstall 13/11/2018 Tim Worstall 13/11/2018 A protectionist is someone who argues that you should be poorer so that they can be richer Read More Madsen Pirie 12/11/2018 Madsen Pirie 12/11/2018 The Power of Capitalism Read More Older Posts Your subscription could not be saved. Please try again. Your subscription has been successful. Blogs by email Enter your email address to subscribe I agree to receive your newsletters and accept the data privacy statement. SUBSCRIBE

Tim Worstall 20/11/2018 Tim Worstall 20/11/2018 Once again, to miss the point about health care treatment costs Read More

Ananya Chowdhury 19/11/2018 Ananya Chowdhury 19/11/2018 An Enquiry Concerning Human Urban Planning Read More

Tim Worstall 19/11/2018 Tim Worstall 19/11/2018 To explain the UN Rapporteur on UK Extreme Poverty Read More

Joshua Curzon 18/11/2018 Joshua Curzon 18/11/2018 Venezuela Campaign: building crisis cements Maduro's failed legacy Read More

Tim Worstall 18/11/2018 Tim Worstall 18/11/2018 Health care is a luxury so of course Americans spend more upon it Read More

Tim Worstall 17/11/2018 Tim Worstall 17/11/2018 What is the correct number of bank branches? Read More

Tim Worstall 16/11/2018 Tim Worstall 16/11/2018 It's the decision making process itself which is wrong here Read More

Tim Worstall 15/11/2018 Tim Worstall 15/11/2018 It's the disinformation from some that so annoys about climate change Read More

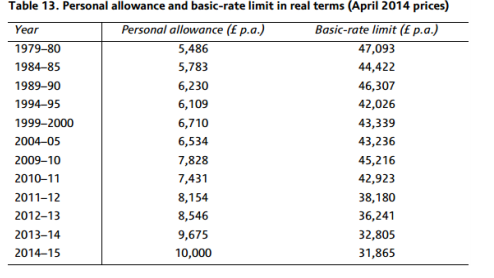

Tim Worstall 14/11/2018 Tim Worstall 14/11/2018 At last, an accurate description of Gordon Brown's personal income tax policies Read More

Tim Worstall 13/11/2018 Tim Worstall 13/11/2018 A protectionist is someone who argues that you should be poorer so that they can be richer Read More