About the Author

Paper

Mitchell Palmer is an Economist at the Adam Smith Institute.

He previously worked as a special advisor to the Deputy Prime Minister of New Zealand, whom he advised on fiscal policy and microeconomics. He has also worked in economic consulting in New Zealand and at a think tank in Singapore.

Mitchell holds a first-class degree in History and Economics from the University of Oxford. While at Oxford, he was made a Hayek Fellow of the Mont Pelerin Society. He also studied at Yale-NUS College in Singapore.

All views expressed in the main body of the paper are those of the author alone.

Foreword

The Rt. Hon. Suella Braverman KC MP is Reform UK’s Shadow Education Secretary and Member of Parliament for Fareham and Waterlooville. She was previously Home Secretary, Attorney-General, and Chair of the European Research Group.

Foreword

Education should be one of the foundations of a nation’s prosperity. For centuries, Britain was seen as a place of learning par excellence, with universities whose ambition to educate recalls the great academies of the ancient world. A degree ought to equip young people with the skills, discipline and ambition to build fulfilling lives and contribute to our country’s future.

But when the funding system that underpins this process becomes opaque, backwards, or unsustainable, confidence is eroded, and the social contract begins to fray. A nation cannot thrive when its young people are burdened by a system that neither rewards effort nor reflects basic economic reality. For too long, education has been seen as a social experiment for Whitehall’s planners, rather than its original role as a foundation stone for national success.

In this thoughtful and rigorously argued paper on the future of England’s student finance system, Mitchell Palmer from the Adam Smith Institute has produced a serious piece of work, one that opens up a much-needed debate about how we fund higher education in a way that is not only fair but prioritises Britain’s national interest by putting our future first.

What stands out in this report is the clarity with which it diagnoses the structural problems that many now agree are fundamental. It cannot be right that the taxpayer is funding graduates being channelled into low-value courses that saddle them with debt and leave them unprepared for today’s world. Nor can it be right that high-earning graduates are disproportionately penalised through the repayment scheme.

The proposed package of lowering interest rates, adjusting thresholds, and extending the write-off period is one possible route to easing the burden on graduates while improving fiscal sustainability. It is not the only path, and this foreword does not endorse any single option since the flawed one-size-fits-all model of higher education has long dominated education-sector thinking. But this analysis provides a strong foundation for further exploration and the radical change that is so desperately needed.

I particularly welcome the report’s willingness to look beyond the confines of the existing failing system. The suggestion that universities should underwrite a portion of loan risk deserves serious consideration, as does the idea of enabling employers to play a more active role in sponsoring study. Those who benefit from higher education, students, institutions, employers and society, should each bear an appropriate share of the cost and risk just as they share in the results.

This paper does not claim to have all the answers. But it asks the right questions, challenges comfortable assumptions that have been accepted for too long and brings quality proposals to a sector that has for too long been dominated by shibboleths. For that, it deserves our close attention and the interest of all those who want to preserve Britain’s position as a global leader in academic excellence.

The Rt Hon Suella Braverman KC MP

Reform UK

Shadow Education, Skills and Equalities Minister

Member of

Parliament for Fareham and Waterlooville

Executive Summary

In her most recent Budget, the Chancellor chose to freeze the income thresholds above which holders of Plan 2 student loans must make repayments. This has reinvigorated a longstanding debate about the fairness, efficiency, and cost-effectiveness of the English student loan system.

In this report, I offer five contributions to this debate.

In Section 1, I estimate the market value of the student loan book and demonstrate that it is materially lower (roughly £33 billion or ~21%) than the book value recorded in the Government accounts. This suggests that the student loan programme is more expensive than is commonly understood and Public Sector Net Financial Liabilities are, in truth, higher than currently thought.

In Section 2, I diagnose some of the problems with the existing loan programme. In particular, I highlight the way it mistargets subsidies to the least-marketable degrees, creates unnecessary anxiety about phantom balances, imposes high effective marginal tax rates on graduates, and is fiscally costly.

In Section 3, I outline how our new model of Plan 2 borrowers works and can be used to estimate the individual-level effects of possible ex-post reforms to the Plan 2 regime. The model is available to use at adam-smith-institute.github.io/student-loan-model. It was used to inform the recommendations made in Section 4.

In Section 4, I make recommendations for how Plan 2 might be reformed to create better value for taxpayers and better incentives for borrowers. I propose that the real interest rate (vs. RPI) should be cut to 0 for all income levels and the repayment rate should be cut to 5%, but the write-off period should be extended to 40 years and the repayment threshold cut by one-third.

In Section 5, I make recommendations for a future student finance system that better shares risks between students, taxpayers, and universities. I propose that new loans should be underwritten by the degree-granting institution to better align incentives and reduce waste. Employees should also be enabled to enter into bonded study funding agreements.

Introduction

Should We Have Student Loans At All?

Before engaging in a detailed discussion about the design and accounting of the student loan system, it is worth understanding why it exists.

The economic justification for government intervention in the provision of student finance is a straightforward market imperfection.1 Unlike traditional lending where tangible assets like property or inventory can be used as collateral, a prospective student’s most valuable asset—their future earnings potential derived from a university education—cannot be pledged as security. Consequently, private lenders face significant uncertainty and risk, as they have limited recourse in the event of default, particularly from lower-earning graduates who may never fully repay the debt. This leads to a situation where private financial markets might either fail to provide sufficient capital for education or do so at prohibitively high interest rates. So-called ‘dynastic financing’ – i.e., from the bank of Mum and Dad – offers a partial solution, but naturally this is not available to all students.

This case for providing finance differs from the case for subsidising higher education. Indeed, it is possible to imagine an unsubsidised student loan system, that solves the financing problem and goes no further, by simply charging a sufficient interest rate to compensate taxpayers for the borrower-friendly nature of the loan contract. Nonetheless, as shown below, the English loan system does include a very large implicit subsidy for higher education.

The case for such a subsidy largely rests on the assumed positive externalities of a university-educated population. This means that many of the benefits of higher education accrue to a third party, so private individuals will buy less for themselves than is socially optimal. I am not convinced that these externalities are in fact large, but most (university-educated and -employed) economists disagree with me, so I will assume that they exist.2 There is also the more subtle point that the taxation of labour income – i.e., the returns on human capital – might discourage even privately-beneficial investment in education. Allowing people to ‘write-off’ their education investment costs from their labour income for tax purposes – or giving them an equivalent subsidy – might be necessary to offset this distortion.

So, there is a prima facie case for both government financing and some level of subsidy. Nonetheless, there remains a question about whether the present – and previous – loan systems were the best way to deliver such a subsidy. The evidence suggests not.

Past and Present

The English student loan system has been substantially reshaped a number of times since its inception in 1990. The ‘mortgage-style’ loans introduced by the Conservative government in that year did what they said on the tin. Students could fund their living costs from this loan and, after graduation, repay it over 60 fixed monthly installments, once their income exceeded a certain threshold. It was debt in the conventional sense of the word.

With the introduction of tuition fees in 1998, the new Labour government introduced a new loan system. These loans can be used to cover both tuition fees and living costs. These new loans featured ‘income contingent repayment’ (ICR), whereby students are never forced to repay more than a given share of their income. They must, however, keep paying this share until either their loan balance is entirely paid off or the loan is written-off by the Government. Though nominally still a debt contract, these new loans are much closer to a capped equity stake in a graduate’s earnings or, indeed, a time-limited graduate tax.

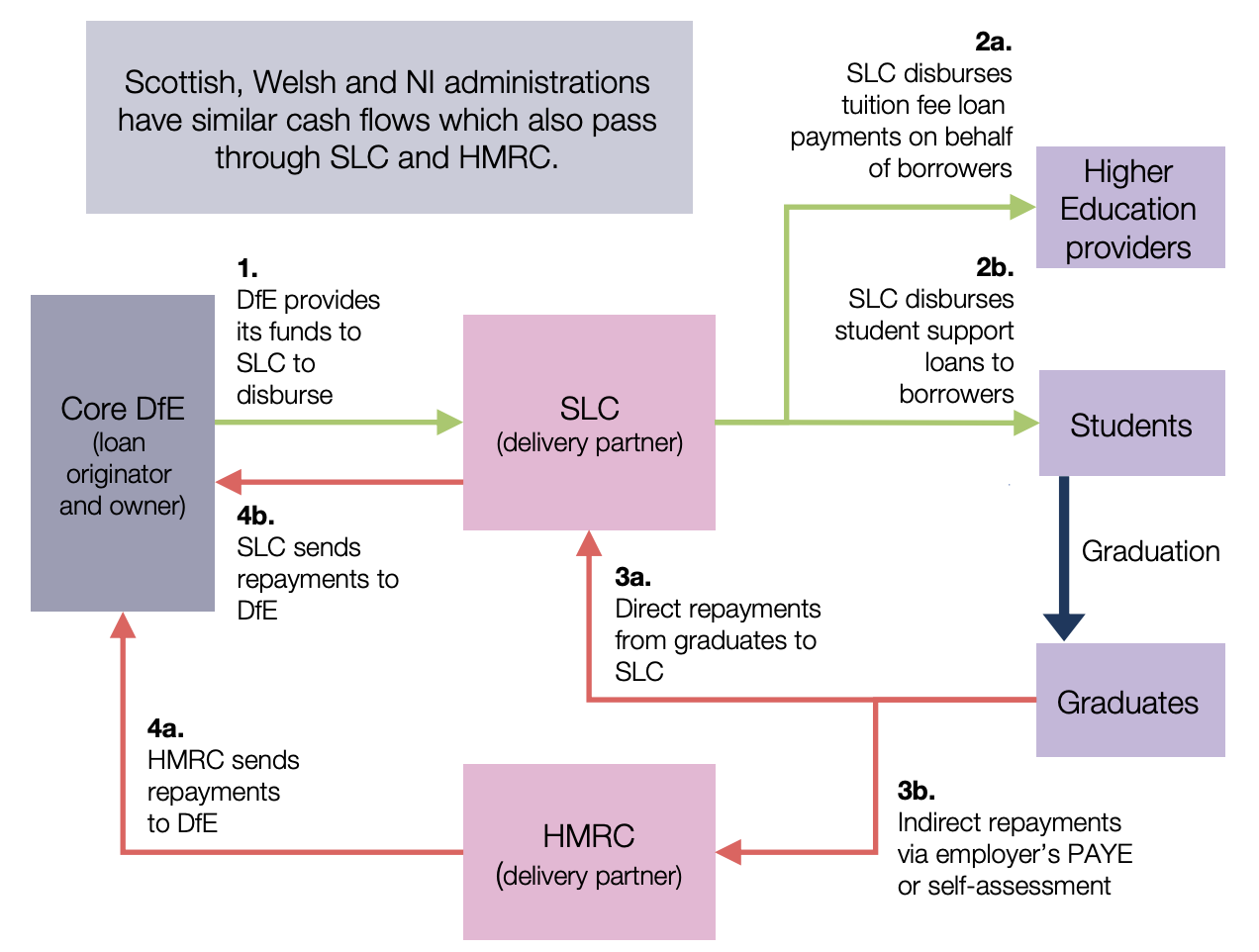

Student loans are issued by the Student Loans Company – which, despite the name, is a public body not administered on a profit-making basis – on behalf of the Department for Education (DfE). Payments are either made to the borrower or direct to the educational institution. Compulsory repayments are collected by His Majesty’s Revenue and Customs through the tax system; voluntary repayments and repayments abroad are made directly to the Student Loans Company. This complex process is shown below in the graph from the DfE annual report.3

Student loans are retained on the Department’s balance sheet and represent around one-quarter of the Government’s financial assets.4 The outstanding loans have a face value of £264 billion, but a carrying value of only £158 billion, which partially represents the very large implicit subsidy included in their design.5

The Plans

Since the introduction of ICR, successive governments have sought to recalibrate the fiscal burden between the taxpayer and the graduate by introducing new ‘plans’. These transitions typically adjust the three primary levers of the system: the fee cap, the repayment threshold, and the repayment term.

| Date | Plan Type | Primary Cohort (England) | Critical Policy Shift |

|---|---|---|---|

| 1998 | Plan 1 | Entrants 1998 to 2011 | Introduction of ICR; annual fees up to £1,000; liability ends at age 65. |

| 2006 | Plan 1 (Revised) | Entrants 2006 to 2011 | Fees increased to £3,000; term adjusted to 25 years after SRDD. |

| 2012 | Plan 2 | Entrants Sept 2012 to July 2023 | Fees increased to £9,000; interest moved to sliding scale (up to RPI+3%); 30-year term. |

| 2016 | Plan 3 | Postgraduate Students | Master’s loans (£10k original); Doctoral loans (£25k original) introduced in 2018. |

| 2023 | Plan 5 | Entrants from August 2023 | Repayment term extended to 40 years; interest rate set at RPI+0%. |

The details of these plans, as they are currently experienced by borrowers, are shown below.

| Feature | Plan 1 | Plan 2 | Plan 3 (Postgrad) | Plan 5 |

|---|---|---|---|---|

| Repayment Threshold | £24,990 (2024/25) | £27,295 (frozen until April 2025) | £21,000 (frozen until April 2026) | £25,000 (fixed until April 2027) |

| Repayment Rate | 9% above threshold | 9% above threshold | 6% above threshold | 9% above threshold |

| Interest Rate | Lower of RPI or Bank Base Rate + 1% | Sliding scale (RPI to RPI+3%), based on income | RPI + 3% | RPI |

Plan 3 postgraduate loans are unusual. Unlike undergraduate loans, they are course-duration entitlements (£12,471 for Master’s and £29,390 for Doctoral courses in 2024/25) that repay concurrently with undergraduate debt. This results in a high marginal repayment rate for many graduates; a borrower with both Plan 2 and Plan 3 loans would repay 15% of their income above the respective thresholds.

To mitigate the impact of excessive inflation, the Department for Education monitors Bank of England data to apply a “Prevailing Market Rate Cap” if RPI-linked rates exceed comparable commercial unsecured loans. Recent caps have been around 8.0% (Aug 2024).

The Effect of Parameters on Borrowers

These parameters matter to borrowers, but in a subtle way. For all graduates, the repayment threshold and rate effectively determine the size of the graduate tax they will pay. But, for low earners, small changes in the interest rate are effectively irrelevant. They will never pay their loan off, so the balance is effectively imaginary. High earners can generally expect to pay off their entire loan, but the rate at which they do is determined by the repayment rules – unless they make voluntary repayments. This means the rate of interest largely determines how long they will pay the ‘graduate tax’.

1. Student Loan Accounting

Student loans are a highly complex financial asset. They are a mixed debt-and-equity claim on the earnings of millions of people, each of whom might get a promotion, die, emigrate, or lose their job at any given moment. Therefore, valuing them is a highly complex process, done using historical evidence on repayment rates and other borrower behaviour. Nonetheless, this effort is worthwhile. As noted above, these loans represent almost a quarter of the Government’s total financial assets. Their valuation therefore has a material impact on the apparent solvency of the British government.

Because student loans are income-contingent, written-off after a given period, and issued at a below-market interest rate, the government treats them as a hybrid of a financial asset and social expenditure. The Resource Accounting and Budgeting (RAB) charge represents the taxpayer subsidy—the proportion of loan outlay that the government expects will never be repaid – and is ‘incurred’ by the DfE in the year that the loans are issued.

The Office for National Statistics (ONS) uses a ‘partitioned loan-transfer approach’ to record this in the public sector finance statistics, splitting each loan into two parts at inception:

- The Financial Transaction: The portion expected to be repaid in full with interest (recorded as a loan asset).

- The Capital Transfer: The portion identified as unlikely to be repaid (recorded as government expenditure immediately).

As noted above, the carrying value of the loans on the DfE balance sheet (and, therefore, the Whole of Government Accounts) was £158 billion, as of March 2025. Using the ONS methodology, the book was valued at £146 billion in the same quarter.6 Both are well below the face value of £264 billion.

Despite these adjustments, neither the ONS valuation nor the valuation recorded in the Department’s accounts really represent the fair value of these loans. Like all financial assets, the student loan book can be – and is – valued as the present value of all of its future cash flows. Such a calculation is highly sensitive to the rate at which future cash flows are discounted to the present.

The discount rates used by both the ONS and DfE are substantially below what the market is likely to demand for an asset like the student loan book. The ONS uses the interest rate of the loans as their discount rate.7 DfE is required to use HM Treasury’s discount rate of RPI minus 0.85% until 2030, and RPI plus 0.05% thereafter.8 That is a nominal rate of around 2.15%. However, the student loan book is a much riskier asset than pure government debt, and this risk is highly correlated with the rest of the economy (i.e., it has a high beta). The Capital Asset Pricing Model therefore suggests that the market would demand a substantial premium above the Government’s cost of borrowing. The yield of a 15-year index-linked gilt (used because it shares the long-term and inflation-protected characteristics of the loan book) is currently around 1.8% above RPI or a nominal yield of around 5.8%.9 A small premium – only 100 bp – would approximately match the discount rate to the average rate of return on UK equities, which seems like an appropriate benchmark. Therefore, we reach an estimated market discount rate of 6.8% or 4.65 percentage points higher than the current DfE assumption.

Unfortunately, DfE does not publish a sensitivity analysis for the effect of the discount rate alone on the value of the loan book. But they do publish ‘multiple factors’ analysis from which it is possible to estimate that a 1 percentage point increase in the discount rate would reduce the carrying value of the loan book by approximately £7 billion (or 4%).10 A 4.65pp change might therefore reduce the value by £33 billion or 21%. This estimate is naturally a rough approximation, because valuations do not respond linearly to changes in discount rates, but it demonstrates the orders of magnitude at stake.

In my view, when we consider the Government’s balance sheet, we should generally mark assets to their market value. That is, we should consider what they might reasonably fetch in an arms-length transaction on the open market. This is because the most important purpose of the Government’s balance sheet is demonstrating the assets available to the Government to meet its current and future obligations to gilt owners, Civil Service pensioners, and the rest of us.

This makes the divergence of discount rates between the Government’s assumptions and the likely market requirement worrying. As demonstrated above, the real value of the book is materially lower than it first appears — and thus, the real level of Public Sector Net Financial Liabilities (this government’s preferred balance sheet metric to target) is materially higher.

Using a market discount rate also more fairly represents the cost of the student loan programme for taxpayers. If a student does not repay their student loan, taxpayers will still have to cover the interest and principal on the additional debt the government borrowed in order to fund that loan. These are real costs that should be recognised when the loan is written and are currently not – because, implicitly, the loan book is assumed to be roughly as safe as government debt.

2. Problem Definition

Leaving aside the accounting, the English student loan system is also riddled with problems that affect borrowers and taxpayers directly.

Mistargeted Subsidies

Firstly, two major features of the ICR loans mean that the effective subsidy given to borrowers and/or degrees with low earning potential is much larger than that given to those whose degrees will have the highest pay-off for both them and society (in purely fiscal terms).

Under ICR, repayments are tied to a borrower’s income rather than the amount they borrowed. Borrowers only pay 9% of their earnings above a specific statutory threshold (currently £28,470 for Plan 2 and £25,000 for Plan 5). Graduates from degrees with low earnings potential may rarely exceed these thresholds, or only exceed them by a small margin, meaning they make very small or zero monthly repayments over their working lives. By contrast, high earners will definitionally make large contributions from the beginning of their careers.

This inequality is then reinforced by the write-off mechanism. The repayment term is 30 years after the Statutory Repayment Due Date (SRDD) for Plan 2, and 40 years for Plan 5. After this point, the outstanding loan balance is completely written off by the government. The government therefore foregoes any further interest or repayments on the balance due. Graduates with low earnings potential are highly likely to reach the end of this term without having cleared their debt, leaving the government to absorb the unpaid balance.

This subsidy narrows the gap between high- and low-earning degrees, which blunts the incentives for students to study marketable subjects. It also means that borrowers are entirely insulated from the risk that their degree will not pay off, which may encourage more of those who should not go to university to go.

Imaginary Loan Balances

Because many borrowers will not make substantial repayments especially in the earliest years of their career, they will likely see a ballooning balance as the interest on a relatively high starting balance accumulates. For the almost 70% of Plan 2 borrowers whom the government does not expect to repay their loan before the write-off date, this is entirely irrelevant.11 Their total repayments are capped at 9% of their lifetime income above the threshold.

Nonetheless, the existence of such a ballooning balance is often deeply demoralising and anxiety-inducing. It also seems to underpin the sense of unfairness that afflicts many recent borrowers, whose already-high nominal balances were further increased by the high rates of inflation (and therefore interest rates) in recent years. This may have damaging political consequences.

High Effective Marginal Tax Rates

The combination of student loan repayments with the tax system creates exceptionally high Effective Marginal Tax Rates (EMTRs) for many UK graduates. An EMTR is the total percentage of an additional pound of income that is taken away by the government through all taxes and income-contingent repayments. EMTRs matter because they shape the incentives for affected graduates to work more hours or seek promotions.

There are five main contributors to the EMTRs for graduates:

Plan 2 and Plan 5 (Undergraduate): Repayment rate of 9% on earnings above their respective thresholds (£27,295 for Plan 2, £25,000 for Plan 5).

Plan 3 (Postgraduate): Repayment rate of 6% on earnings above the £21,000 threshold.

Income Tax: 20% on income between the PA limit (£12,570) and the Higher Rate threshold (£50,270); 40% up to £125,140.

Employee National Insurance: 8% on weekly earnings between £242 and £967 (approximately £12,584 and £50,284 annually); 2% thereafter.

Personal Allowance withdrawal: The £12,570 personal allowance is reduced by £1 for every £2 of adjusted net income over £100,000. This creates an effective marginal tax rate of 60% on income between £100,000 and £125,140: the 40% Higher Rate Income Tax plus a 20% implicit tax (as the withdrawal of the PA makes an extra 50p of income taxable at 40% for every £1 earned).

Some graduates may also face the earnings taper of their benefits, such as Universal Credit, which further increases the EMTR on labour income.

A graduate with both Plan 2 (or Plan 5) and Plan 3 loans simultaneously paying the basic rate of income tax and the main rate of NICs faces an EMTR of 43%, despite a relatively low income level. Even with an undergraduate loan alone, they face an EMTR of 37%. Because such a borrower is unlikely to pay off their loan before it is written off (especially under Plan 2), they are likely to face this situation for their entire working life.

But they are not the worst afflicted. If a graduate with a post-graduate loan ends up in the dreaded £100,000 trap, they could face an EMTR of 77%, made up of 40% income tax + 20% PA withdrawal + 2% NICs + 9% UG loan + 6% PG loan. Less than ¼ of their marginal income would hit their back pocket. Luckily, for such an earner, they are likely to repay their loans very quickly and be set free from 15 percentage points of this burden. Nonetheless, this will have a severe impact in the interim.

Excessive Fiscal Costs

As noted above, the student loan system features large implicit subsidies that are poorly targeted. These come at a substantial cost to taxpayers. Some of this cost is recognised when the loan is issued – through the RAB charge or ONS loan-partitioning – but as noted, the chosen discount rate understates how large these costs are.

Still, the RAB charge is large. Even under the better-designed Plan 5 system, of the £15,450 borrowed by an average full-time undergraduate borrower in 2024/25, £4,480 was immediately written-off as subsidy.12 Aggregating across all borrowers, the cost is around £7 billion a year, which is roughly 7% of the total education budget.

3. Model Introduction

In order to demonstrate these flaws – and how policy changes may affect them – I have built a simplified model of a hypothetical borrower. It can be used at adam-smith-institute.github.io/student-loan-model. The model follows the lifetime trajectory of an English Plan 2 student loan — the scheme covering graduates from 2012 to 2023. It allows users to adjust both the characteristics of the hypothetical borrower and the parameters of loan policy, then compares a “status quo” scenario against a user-defined “changed” scenario side by side.

The core output is a year-by-year simulation of loan balance, interest accrued, and repayments from the borrower’s graduation through either full repayment or write-off. From these cash flows the model derives summary statistics including total repaid, total interest, and the year of payoff or write-off. It also produces net present value (NPV) estimates under three different discount rate conventions — Government/HMT, Market, and ONS/borrower rate — as well as the RAB charge, which represents the effective government subsidy expressed as a fraction of the loan’s face value.

Key Assumptions

Income and Career Trajectory

The borrower is assumed to begin work in their graduation year at a user-specified starting salary. Income then grows each subsequent year through two compounding factors applied simultaneously. The first is an age-dependent real career growth rate derived from empirical earnings profiles: workers in their early twenties see strong real wage growth (around 2.4% per year for ages 22–29), which tapers to near zero in the thirties and turns mildly negative after forty, reaching around −1.3% per year for workers over fifty. The second factor is economy-wide nominal wage growth, proxied by the Average Weekly Earnings (AWE) index, which shifts all incomes in line with the broader labour market each year.

The model assumes the borrower is continuously and fully employed throughout their working life. There is no provision for unemployment spells, career breaks, part-time work, or early retirement.

Macroeconomic Series

RPI inflation is taken from historical data through 2025, then assumed to run at approximately 3% per year through 2029 before settling at a long-run rate of 2.1% per year from 2030 onward. The AWE series similarly uses historical data through the mid-2020s and then extrapolates forward at the most recently observed growth rate.

Repayment thresholds — both the lower threshold (below which no repayment is due) and the upper threshold (above which the maximum interest rate applies) — are taken from published government figures where known, and projected to grow in line with RPI once the published series runs out.

Interest Rate Mechanics

While studying, the borrower is charged the high interest rate, which is RPI plus the high spread (3% by default). After graduation, the interest rate tapers linearly with income: borrowers earning at or below the lower threshold are charged RPI plus the low spread (0% by default), while those at or above the upper threshold are charged RPI plus the high spread. Borrowers with income between the two thresholds pay a proportionally interpolated rate.

During the period from 2021 to 2024, the government imposed a Prevailing Market Rate (PMR) cap on student loan interest. The model accounts for this by computing a weighted average of the capped rate (applied in months where the cap was binding) and the uncapped formula rate (applied in remaining months) within each affected tax year.

Loan Balance Mechanics

The loan balance accumulates during study from annual tuition fees and maintenance loans (or, alternatively, can be entered directly as a known 2025 balance). After graduation, annual repayments are calculated as 9% of income above the lower threshold — the standard Plan 2 rate — subject to a cap that prevents repayments from exceeding the outstanding balance plus accrued interest in any given year. Any remaining balance is written off after the write-off period, which defaults to 30 years post-graduation.

Valuations and Discount Rates

The model computes NPVs from 2026 onward under three discount rate conventions. The Government/HMT rate approximates the government’s cost of borrowing: RPI minus 0.85 percentage points before 2030, transitioning to RPI plus 0.05 percentage points thereafter. The Market rate uses a fixed 6.8% per year, reflecting a private-sector opportunity cost. The ONS/borrower rate discounts at the borrower’s own interest rate each year, which corresponds to the methodology used by the Office for National Statistics in its student loan valuations.

The RAB charge — the Resource Accounting and Budgeting charge — is derived from the HMT valuation as the share of the loan’s face value that is not expected to be recovered in present value terms. A RAB charge of, say, 40% means the government expects to recover only 60 pence in present value for every pound lent.

What the Model Does Not Capture

The model is deliberately simplified and is not intended as a precise predictor of individual outcomes. It does not model income volatility, unemployment, or part-time work; it does not account for tax interactions such as National Insurance or income tax; and it does not capture any behavioural responses to policy changes. It is a single-borrower model and does not aggregate across cohorts to produce fiscal cost estimates. The model covers Plan 2 only and does not apply to Plan 5 (post-2023 entrants) or other loan plans.

4. Recommendations for Plan 2

The vast majority of current loan balances (81%) are under Plan 2. They were accrued by students entering the system from September 2012 to July 2023. Moreover, it is these loans that are the subject of the most complaints. It is therefore the obvious target for reform. Making alterations to the loans that people have already committed to may seem unfair. Nonetheless, these are effectively a tax product, and they have already been altered substantially. Thus, making further changes to make the loans fairer on taxpayers and borrowers is consistent with the history and nature of the product.

As noted above, valuing the student loan book – and therefore determining the exact fiscal consequences of policy reforms – is very complex. Nonetheless, it is possible – using the new ASI model – to determine the effects of proposals on representative borrowers. This will give a sense for the direction and magnitude of the likely aggregated fiscal cost of any given proposal. In particular, we have looked at the effects on three borrowers, differentiated only by their starting salaries (£16,000, £25,000, and £50,000). These borrowers are assumed to be otherwise identical: Graduating in 2018, following the standard lifecycle pattern of relative earnings, and with 3 years of undergraduate education and £3,900 in maintenance loans each year.

Lower Interest Rate

To deal with the damaging psychic impact of ballooning debt balances, I propose lowering the Plan 2 interest rate to RPI, regardless of income, down from RPI+3% for those over the higher earnings threshold and a rate between RPI and RPI+3% for those above the repayments threshold. On its own, such a change will have no economic effect on low- and middle-income borrowers as it will probably not be sufficient to ensure they repay the entire loan in the 30 year term. It will therefore largely be a lump-sum transfer to higher earners, allowing them to repay their loans quicker. Still, this is worthwhile as it will reduce the EMTRs on such earners later in their career and reassure other borrowers that their nominal ‘debt’ is not spiraling out of control.

This proposal has no impact on the carrying value (or net present value/NPV) of our low earner’s loan, because he never earns enough to make a substantial repayment, under any discount rate. Similarly, it has no economic impact on our mid-tier earner, who makes substantial repayments but never repays his entire loan. Nonetheless, for the mid-tier earner, it will substantially reduce the closing balance. For our high earner, this change reduces the carrying value of his loan by 12% at market rates and 13% at HMT’s discount rate. It has no effect on the ONS valuation, because this discounts the loan at the borrowers’ interest rate, so the reduction in repayments is exactly offset by the lower discount rate.

The total fiscal consequences of this proposal in isolation are therefore likely negative, but only mildly so, because only a relatively small percentage of Plan 2 borrowers are expected to repay their full loans in the 30 year term.

Lower Repayment Rate and Lower Repayment Threshold

To deal with the high EMTRs that many borrowers will face, it makes sense to reduce the repayment rate. However, this would be very fiscally expensive. Therefore, it can be offset by also reducing the level of income at which repayments must be made. This will reduce the income insurance implicit in the student loan contract. This insurance helps to protect borrowers from adverse income shocks, such as unemployment, but it also insulates them from the real economic consequences of their decisions. Reducing the insurance will ensure that those who undertook unmarketable degrees will bear some of the cost of their education. Naturally, it will also make the system less progressive, but the British income tax system is quite progressive by European/OECD standards, so this is not necessarily a problem.13 I propose a 5% repayment rate (down from 9%) and a repayment threshold still indexed to RPI, but cut by ⅓.

In isolation, this proposal increases the carrying value of the higher earners’ loan by 63% (HMT rates) and 27% (market rates), while reducing his marginal and average repayment rates. It achieves this by lengthening his repayment term. For the middle earner, this proposal (in isolation) reduces the carrying value by a bit over 10%, while substantially reducing his marginal and mildly reducing his average repayment rates. It has no impact on the repayment term, which is still determined by the write-off date. For the low earner, this proposal substantially increases his marginal and average repayment rates, from zero to 5% and around 1.5% respectively. Because this borrower will now make repayments, it increases the NPV of his loan from approximately 0 to 18% of its face value (HMT rates) and 11% (market rates).

The fiscal consequences of this proposal are therefore ambiguous. It depends whether the effects of newly collecting repayments from low earners and lengthening the term of high earners’ loans are sufficient to offset the mild repayment relief for middle earners.

Longer Write-Off Period

To offset the fiscal costs of these reforms and more fairly allocate the burden of education costs between high- and low-earners, it makes sense to extend the write-off period to 40 years, or the entirety of the foreseen working lives of graduates. This aligns more closely with the practice in other countries. In Australia, New Zealand, and Canada, student loan debts are only written-off at death. The rationale for a write-off before retirement is difficult to understand – a student should theoretically still be enjoying the consequences of their degree through their entire working life and, if anything, additional disposable income is likely to be more valuable earlier in life, when overall earnings are typically lower and/or it can be profitably invested.

In isolation, lengthening the write-off period has little impact on our high- or low-earner. The high earner’s loan is forecast to be repaid by 2034 (i.e., 16 years after graduation), and the low earner is never expected to earn enough to make substantial repayments. The middle income earner will, however, pay substantially more of his loan back. Nonetheless, these repayments will be made in the distant future, so they are discounted quite heavily. Still, the NPV of his loan will increase by 40% at HMT’s discount rate and 21% at market rates. Thus, the combined fiscal effect of lengthening the write-off period is unambiguously positive.

Combined Package

Because these three proposals interact with each other strongly (e.g., lowering the repayment threshold means that the low earner will now make repayments for the newly-lengthened term of the loan), their combined effects are not simply the sum of their individual effects.

A full package of a lower interest rate, a lower repayment rate, a lower repayment threshold, and a longer write-off period would likely be strongly fiscally positive. The NPV of the high earner’s loan would increase by 20%/4% at HMT/market rates, the middle earner’s loan NPV would increase by 24%/6%, and the low earner’s loan NPV would go from close to 0 to £14,782 (HMT) or £7,564 (market) – or 26%/13% of face value.

5. Recommendations for a New System

These changes will improve the fiscal sustainability and fairness of the existing Plan 2 loans. Indeed, they will make Plan 2 largely resemble the Plan 5 loans that are currently being issued to new students. Plan 5 is much better designed, but it is still not perfect. In particular, it features no attempt to ‘underwrite’ the loans, so that taxpayer financing and subsidies go to the borrowers most likely to repay their loans and/or the educational investments most likely to provide value to society.

Governments have some information available to them to make educated guesses about this. In particular, they now have data on the repayment trajectories of millions of past borrowers. In Australia, the Government uses this data and others to allocate and price ‘Commonwealth Supported Places’ at universities, especially for postgraduate degrees. Still, this is an imperfect way to predict the future. Better, in my view, to allocate the risk of non-repayment to those people best able to minimise it. There are three obvious candidates: The institution itself, employers, and students.

The detailed design of a new student finance system is a matter for another paper, but it is worth briefly discussing some alternative options.

Institutional Underwriting

Requiring institutions to take some of the risk of their students’ low earnings (and the upside of their students’ high earnings) would encourage them to (1) admit only those students likely to succeed, (2) prioritise degree programmes with strong employment outcomes, and (3) invest heavily in the job preparation of their students.

There are important questions about how to structure such a university-led financing program. Even the best British universities are not especially well-endowed, so they likely cannot be expected to front student fees themselves and collect them back gradually over the students’ career. Instead, universities might be able to enter into financial transactions with banks to front them with funding for these loans. The residual risk of repayment could remain on the institution’s balance sheet – or be reflected in an upfront discount from the bank. The government might also step in to provide some additional subsidy, to share some (but not all) of the risk.

Such a model would almost certainly make many British universities financially inviable. This is not necessarily a bad thing. If a university consistently produces students that cannot fund their degrees through higher earnings, they are wasting students’ and academics’ time alike. And insofar as university courses have value beyond a mere investment in human capital, this is a form of consumption. It is unclear why it should be subsidised more than other types of consumption.

Employer Participation

Employers could also play a useful role in financing higher education. By providing both the education and the eventual job, they can eliminate uncertainty for themselves about their pipeline of staff and uncertainty for borrowers about their employment prospects. Such a model is already used effectively by the military and implicitly by the NHS, through very large subsidies for medical education. It is also used in the legal profession to fund law conversion courses and professional examinations.

However, because degrees cannot be repossessed, private sector employers face a strong risk that their freshly-trained graduates will leave, before they ‘pay back’ a return on their investment. It is naturally in the interests and capability of competitors to do so, as they will be able to pay the worker their true marginal product of labour without deducting an (implicit) allowance for education costs. Historically, guild systems prevented this by ensuring that apprentices would stay with their trainer/employer for a reasonable period. Before large-scale emigration of doctors became a problem, the NHS’s effective monopoly allowed it to act similarly with impunity. But in a competitive labour market, such collusive agreements are likely impossible (or perhaps illegal and definitely undesirable) to sustain.

A training bond, whereby an employee is always at liberty to leave his employment early but must pay back his training costs if he does so, can theoretically solve this problem. Such training bonds are legal in the United Kingdom, but they are subject to strict limits.

A standardised structure for employer-backed loans could perhaps work. The primary employer could select a future employee to fund and advance that employee funding for a degree to be collected from his paycheque upon employment. This loan could accrue interest at a low rate, but also be purchasable out-right by the employee or also a future employer. This would assure the employer of a reasonable return on his investment, without trapping the employee in a job that was not right for him.

Price Signals

Loosening the price cap on university course fees could also allow for students to make choices about whether a particular course is a useful investment. At present, the price cap effectively forces cross-subsidation between different degree programmes, undermining the incentive for students to pick cost-effective, high-return courses.

However, the price cap does serve a useful purpose in the context of highly subsidised loans, where the subsidy increases with the amount borrowed. Given these subsidies, low- and middle-earning students face no incentive whatsoever to economise, so universities could (in the absence of a cap) set arbitrarily high prices, meaning the loan system would effectively be a very large transfer from taxpayers to universities. If however borrowers bore a larger portion of their own education costs, the price mechanism could be allowed to function.

Conclusion

The English student loan system, particularly Plan 2, is structurally flawed. It imposes excessive fiscal costs on the taxpayer, creates perverse incentives, and causes undue anxiety for borrowers. The de facto market value of the loan book is also significantly lower than its recorded value in government accounts, implying that the true cost to the Exchequer is systematically understated.

The current income-contingent repayment (ICR) mechanism, coupled with the write-off period and the high EMTRs it creates, operates less as a debt instrument and more as a mistargeted graduate tax. Critically, it subsidizes degrees with lower market returns and penalizes high-earning graduates, thereby dampening incentives to invest in high-return education and labour.

To address the immediate failings of the Plan 2 system, I recommend a combined reform package: lowering the real interest rate to RPI for all borrowers to reduce psychological debt burdens, cutting the repayment rate to 5% to ease EMTRs, but offsetting the fiscal cost by cutting the repayment threshold by one-third and extending the write-off period to 40 years. My modeling demonstrates that this package would be fiscally positive, increasing the Net Present Value of loans across low, middle, and high earners, while simultaneously creating fairer incentives.

Further into the future, we should consider bolder reforms. The new system should not allocate all of the risk of a dud degree onto taxpayers. I propose exploring models where universities underwrite a portion of the loan risk to improve accountability and course quality, and where employers are facilitated to offer bonded study funding agreements. Finally, allowing the price mechanism to function through loosening the fee cap, provided that borrowers bear more of the true cost of their education, would promote greater efficiency and reduce the current reliance on poorly-targeted taxpayer subsidies.

The current system masks the cost of higher education through opaque subsidies and ballooning imaginary balances. Our goal should be to create a student financing system that is transparent, fiscally sustainable, and aligns the incentives of students, universities, and taxpayers to deliver real value for graduates and society.

For the clearest statement of this argument, see Milton Friedman, ‘The Role of Government in Education’ (1955).↩︎

For the sceptical side of this argument, see Bryan Caplan, The Case Against Education (Princeton University Press, 2018).↩︎

DfE Annual Report 2024/25, p. 304.↩︎

DfE Annual Report 2024/25, p. 305-7.↩︎

ONS, ‘Public Sector Finances Bulletin, January 2026’, Appendix O, code J6GI.↩︎

Author’s calculation; data from Student Loans Company, ‘Student Loans in England: Financial Year 2024-25’.↩︎

N.b., the calculation method for RPI will change in 2030, which will bring it closer to CPI’s long-term targetted average of 2%.↩︎

As of 20 February 2025.↩︎

See DfE Annual Report 2024/25, p. 254. Full calculations available in the PDF version of this report.↩︎

House of Commons Library, ‘Student loan statistics’ (2025)↩︎

Department for Education, ‘Student loan forecasts for England, FY 24/25’.↩︎

To demonstrate this, compare the top rates in the UK to the average tax wedge for a median earner. According to the OECD, the UK’s tax wedge for the average single worker in 2024 was 29.4% (vs the OECD average of 34.9%). Meanwhile, the UK’s top income tax rate is 47%, compared to the OECD average of 46%.↩︎